FY26 update - Plenti more than doubles Cash PBT

Highlights

- FY26 Cash PBT of $30.8 million and FY26 Cash NPAT of $27.3 million,representing growth on FY25 of 117% and 97% respectively

- All FY26 objectives for growth, profitability and efficiency delivered

- FY26 originations of $1,868 million, up 32% on PCP

- Loan portfolio increased to $3.1 billion, up 22% on PCP

- Strong credit performance with annualised net losses of 94 basis points

- Generated $20.6 million ofcorporate cash, allowing $12.5 million repayment of corporate debt

Operational highlights

- Reduced operating cost-to-net margin to 56.7%, from 60.7% in PCP, evidencing theoperating leverage inherent in Plenti’s digital platform-led business model

- Continuedto advance Plenti’s proprietary platform with significant AI-drivenenhancements and material improvements in straight through processing rates(enabling ‘no human touch’ within the PL application to approval process)

- Completed three ABS transactions for total annual issuance of $1.4 billion, taking totalABS issuance since program inception to over $4.7 billion across twelvetransactions

Strategic highlights

- Achieved “Horizon 1” objective of $3 billion loan portfolio in January 2026, ahead of the original 31 March 2026 target

- Transitioned into Horizon 2 of Plenti’s corporate strategy, with continued focus ondisciplined, profitable growth across Plenti’s three core lending verticals andan expanded ambition for accelerated growth in commercial automotive lending through

- The launch of a refreshed product offering and the targeting of a broader end marke

- Strengthened engagement with specialist commercial asset finance aggregators and broker networks

- The launch of a refreshed product offering and the targeting of a broader end marke

Adam Bennett, Plenti’s CEO, said:

“FY26 was a year of strong delivery for Plenti, with the team executing on every element of our FY26 objectives and reaching the $3 billion loan portfolio milestone well ahead ofschedule.

Our proprietary digital. platform, our diverse and complementary distribution channels, and our disciplined credit decisioning combined well to deliver growth in Cash PBT to $30.8million, an increase of 117% on the prior year. This profit growth demonstrates the operating leverage inherent in our digital business model, the talent anddiscipline of our team across originations, credit, technology and funding, and the growing cash generation capability of the business.

With Horizon 1 of our corporate strategy successfully delivered, we now move into Horizon 2 with strongmomentum across our Automotive, Renewables and Personal Lending verticals andan expanding set of AI-enabled capabilities. Whilst we’ll increase investment and focus on these existing verticals, we’ve also relaunched our Commercial Auto proposition to take advantage of the huge market opportunities that exist in this segment. I’m extremely excited about the year ahead as we continue to make progress towards our medium-term ambition of reaching a $5 billion loan book.”

Loan portfolio and revenue growth

Plenti’s diversified loan portfolio increased to $3.1 billion at 31 March 2026, up 22% from the prior comparable period (PCP). The growth in Plenti’s loan portfolio drove revenue to $312 million, up 20% on PCP.

Loan originations by lendingvertical

Total loan originations for FY26were $1,868 million, up 32% on PCP, representing a record annual result for the business. Plenti continued to drive loan origination growth by:

- Leveraging the flexibility and speed of its digital platform to adapt to changing market conditions and capture emerging opportunities

- Continuing to develop fast, easy and simple digital experiences for customers

- Building on deep, diverse and complementary relationships with valued brokers and strategic partners including NAB, Tesla and AGL, whilst adding exclusive administration of the Western Australia Residential Battery Scheme

- Maintaining disciplined underwriting, credit decisioning and operations management

Loan origination momentum remained strong throughout the year, with each quarter of FY26 delivering growth on PCP and 4Q26 settingan all-time record for the value of daily loan originations.

All lending verticals contributed meaningfully to the full year result:

- Automotive loan originations were $994 million, up 40% on PCP, reflecting ongoing growth in Plenti’s consumer and commercial automotive verticals and the scale-up of the NAB powered by Plenti product

- Renewable energy loan originations were $239 million, up 26% on PCP, supported by continued adoption of solar and battery solutions and Federal and State government incentive programs (including the WA Residential Battery Scheme)

- Personal loan originations were $636 million, up 23% on PCP, with growth supported by continued investment in digital acquisition channels and increasing levels of API-integrations with key referral partners, together with further advancements in automated “straight-through-processing” to increase speed of credit application review and approvals

Technology enhancements

Plenti continued to invest in its proprietary digitalplatform during the year, with significant focus on customer experience, creditdecisioning, pricing, partner integrations and operational efficiency.

A particular highlight was the deployment of multipleAI-driven initiatives across the business, supported by Plenti’s end-to-endcontrol of its technology environment. These included a new front-end digitalloan journey designed and deployed 70% faster than Plenti’s historicalbenchmarks using AI-assisted development tools; an AI enabled verificationengine, which assessed over 35,000 customer and partner-supplied documentsduring 4Q26 alone; and a new agentic AI platform supporting customer service,sales engagement and broader process automation.

Consistent with prior years, all product and technologyspend, which amounted to $15.9 million in the year, was expensed through theprofit and loss statement, rather than being capitalised on the balance sheet.

Credit performance

Plenti delivered another year of strong credit performance, reflecting the prime nature of its loan portfolio. Full-year netrealised credit losses were low at 0.94%, down from 1.10% in PCP. 90+ dayarrears were 0.42% at the end of the period, broadly stable on 0.43% at the endof PCP, again reflecting the credit quality of Plenti’s portfolio and ongoing refinement of credit rules. Lower-risk secured automotive and renewable energy loans together represented approximately 71% of the loan portfolio at the endof the period, broadly consistent with PCP.

Plenti remains alert to the potential creditimplications of recent geopolitical and macroeconomic developments, butbelieves that its disciplined approach to credit, combined with its strong prime loan portfolio and market segment diversification, position the business wellin less certain economic conditions.

Margins, costs and profitability

Plenti’s net interest margin for FY26 was 5.45%, up14bps on PCP. The margin result was pleasing given ongoing increases in market funding costs through the second half of the year. The average loan portfolio marginwas substantially supported by attractive pricing outcomes across ABS transactions executed and warehouse extensions.

Plenti continued to demonstrate the operatingleverage inherent in its technology-led business model. Operating cost-to-net margin for FY26 reduced to 56.7%, from 60.7% in PCP and below the 57% targetthreshold. Operating costs for FY26 were $73.8 million, up 19% on PCP against27% growth in net margin, evidencing operating leverage as the loan portfolioscales.

Cash PBT for FY26 of $30.8 million represented anincrease of 117% on PCP, and Cash NPAT of $27.3 million an increase of 97% onPCP, reflecting strong portfolio growth, disciplined cost management and the continuedstrength in Plenti’s credit performance.

Financialposition and funding

Plenti continued to scale and diversify itswell-established funding platform during the FY26 year with the Treasury teamdelivering very strong results to support business growth and profitability.

Conducive debt market conditions, combined with Plenti’sstrong 10+ year credit history, enabled Plenti to complete three ABStransactions during the year for a total of $1.4 billion at the lowest weightedcost of funds since 2021.

In October 2025, Plenti established an additionalmulti-product warehouse with efficient pricing and capital parameters, addingincremental funding capacity and enhancing margins on new lending.

FY26 was also a watershed year for corporate cashgeneration driven by the significant growth in business profitability as wellas efficient loan portfolio funding outcomes. Plenti generated $20.6 millionincremental corporate cash, post funding growth in the loan portfolio. Thismeaningful cash generation allowed $12.5 million of corporate debt to be repaidin March 2026, reducing the drawn facility balance to $20 million. Available corporatecash at 31 March 2026 was $34.6 million (excluding $24.0 million in customercollections accounts). This was up $8.1 million from the available corporate cash balance at 31 March 2025 of $26.5 million.

Plenti has recently established an Employee SharePlan Trust to help facilitate its employee equity plans. Given the availabilityof corporate cash and the current financial position, Plenti intends to usethat Trust to acquire up to a maximum of $3m of shares on market that will thenbe used to satisfy some of its obligations to participants in those plans.

NAB Partnership – Commercial Terms Variation and RenewablesUpdate

Continued momentum in 4Q26with the ‘NAB powered by Plenti’ car loan saw average originations per businessday increase 35% on prior quarter and the loan portfolio increase to $121 million at 31 March2026, up 34% on the prior quarter.

Plenti and NAB brought forward their scheduled review of the car loan partnership. To support greaterinvestment in growth activities by NAB to drive higher origination volumes, Plenti has agreed to some changes as follows:

- Bringing forward of the scheduled step down in the upfront fee per loan funded, and removal of the associated guaranteed minimum monthly value of the per loan upfront fees, thereby also removing the minimum annual revenue amount to be received by Plenti under the strategic partnership

- A reduction in the level of the monthly servicer fee and subsequent schedule for scaling down of the servicer fee as the loan portfolio grows

- The revised terms also provide greater flexibility for both parties to invest in mutually beneficial marketing and promotional campaigns for growth

Related to these amendments,distribution of the ‘NAB powered by Plenti’ car loan will be expanded into NAB’sbanker assisted channels over coming months. In addition, the RenewablesReferral program, previously announced as part of the NAB strategicpartnership, is anticipated to launch to NAB's homeowner customer base during Plenti’s1HFY27.

Horizon 2

Plenti completed Horizon 1 of its refreshed corporatestrategy (“GROW by doing what we do, but better”) during FY26, delivering onthe $3 billion loan portfolio milestone ahead of schedule.

The business has now transitioned into Horizon 2 (“GROW by also doing newthings”, April 2026 to March 2028).

The three key elements of Plenti’s corporate strategy which will be pursued across all three horizons are to:

- Strengthen relationships withtarget customers and partners to ensure complementary and diverse distributionchannels.

- Enhance the use of data andartificial intelligence to improve credit decisioning, reduce the cost of service,optimise pricing, and substantially uplift new customer originations andcross-sell capabilities.

- Leverage Plenti’s proprietarydigital platform to provide customers and brokers with one of the fastest,easiest, simplest lending experiences available in market.

In Horizon 2, Plenti willcontinue to prioritise profitable growth across its core Automotive, Renewablesand Personal Lending verticals, whilst also pursuing strong growth inCommercial Auto through the launch of a refreshed product offering and thetargeting of a broader end commercial automotive market, coupled with strengthenedengagement with specialist commercial asset finance aggregators and brokernetworks.

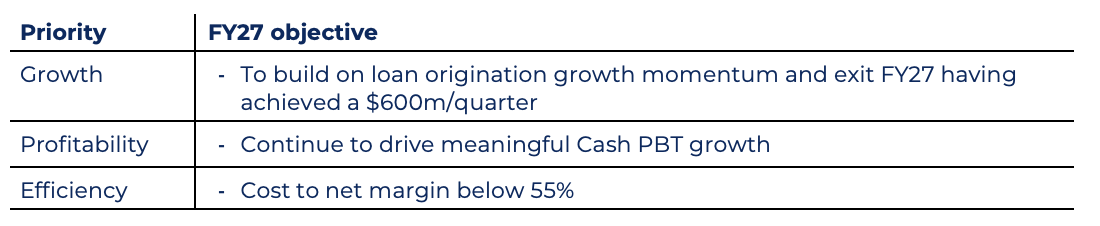

FY27 objectives

Plenti’s objectives for the year to 31 March 2027 areset out below:

CFO transition

Following Miles Drury stepping down as CFO on 22 May2026, Tom Wright, General Manager Strategy Execution, will act as CFO on aninterim basis, ahead of Selena Verth commencing in July 2026, as outlined inPlenti’s February announcement.

Changeof registered office address

Plenti advises that, in accordance with ASX ListingRule 3.14, effective 1 June 2026, the Company’s registered office and principalplace of business will change to:

Level 19, 123 Pitt Street, Sydney NSW 2000

The Company’s contact number and email addressesremain unchanged.

Note:Plenti loan portfolio and origination numbers in this release include “NABPowered by Plenti” automotive loans