4Q26 update - Plenti delivers record $30.8m Cash PBT

Financial highlights

- Unaudited full year FY26 Cash PBT of $30.8 million and unaudited FY26 Cash NPAT of $27.3 million, representing growth on FY25 of 117% and 97% respectively

- All FY26 market guidance objectives for growth, profitability and efficiency delivered

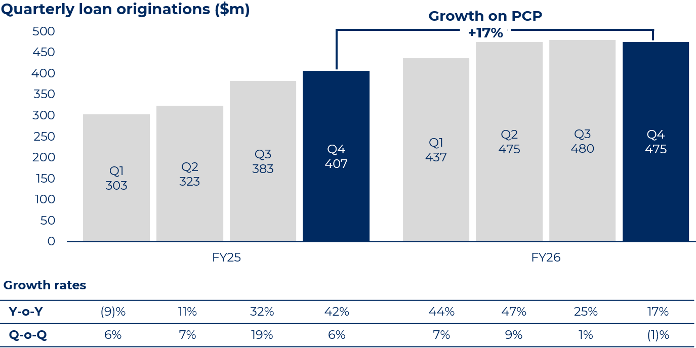

- Quarterly originations of $475 million, up 17% on PCP and broadly consistent with the prior quarter, with fewer business days this was an all-time record for daily originations

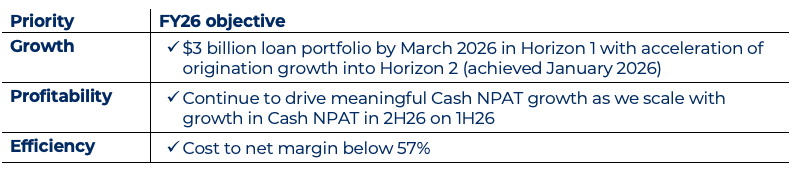

- Loan portfolio increased to $3.1 billion, up 22% on PCP and up 4% on the prior quarter, achieving the FY26 target of a $3 billion loan portfolio in January 2026, well ahead of the original 31 March 2026 deadline

- “NAB powered by Plenti” loan portfolio increased to $121 million, up 34% on the prior quarter, with daily origination run-rate up 35% on the prior quarter

- Strong credit performance with annualised net losses of 96 basis points and 90+ day arrears of 42 basis points at quarter end, stable on the prior quarter and down from PCP

- Continued to drive customer experience and efficiency through technology, including numerous AI deployments across the business

- $400 million PL & Green ABS transaction completed, achieving Plenti’s best pricing for any PL &Green transaction to date with a record number of investors participating

- Repaid $12.5 million of corporate debt, reducing corporate facility to $20 million

Commenting on the quarter, Adam Bennett, Plenti’s Chief Executive Officer said:

“I’m delighted to close FY26 with another strong quarter, maintaining growth momentum by leveraging Plenti’s proprietary digital platform across our diverse channels to market. Total originations of $475 million was a robust result in a more variable operating environment and helped us materially exceed our original year-end loan portfolio target of $3 billion, with portfolio growth of 22% year-on-year.”

“Our full year Cash PBT and Cash NPAT results were a particular highlight, as our disciplined delivery drove significant profitability growth, and this in turn generated surplus free cash to repay corporate debt and fund ongoing loan originations.”

FY26 objectives

Plenti is pleased to have successfully delivered on its three FY26 objectives across growth, profitability and efficiency.

Plenti achieved unaudited Cash PBT of $16.7 million in 2H26, bringing full year FY26 unaudited Cash PBT to $30.8 million, an increase of 117% on PCP. Unaudited Cash NPAT in 2H26 was $14.5 million, resulting in full year FY26 unaudited Cash NPAT of $27.3 million. This represents growth of 97% on FY25 Cash NPAT of $13.8 million.

Plenti’s strong originations momentum throughout FY26saw the delivery of the $3 billion loan portfolio objective ahead of the original target of January 2026.

Unaudited operating cost-to-net margin for FY26 was56.7%, below the target threshold of 57%.

Further details in respect of FY26 and the outlook for FY27 will be provided when Plenti reports its full financial year result on Wednesday 20 May 2026.

Loan portfolio

Plenti’s loan portfolio, which is a key driver of revenue and profitability, increased to $3.1 billion at 31 March 2026, a 22% increase from 31 March 2025 and a 4% increase from 31 December 2025. The loan portfolio remains diversified across Plenti’s three lending verticals, each of which delivered strong growth against the prior corresponding period (PCP) and prior quarter.

Loan originations and margins

Overall originations result

Plenti delivered loan originations in the quarter of $475 million, up 17% on PCP and broadly consistent with the prior quarter.After adjusting for the number of business days in the quarter, originations were up approximately 1% on the prior quarter, achieving an all-time record daily rate for Plenti. FY26 originations of $1,868 million represent growth of32% on PCP, a record annual result for the business.

Product level originations

Automotive loan originations were $251 million, up 29% on PCP and up 1% on the prior quarter. This result reflected ongoing growth in Plenti’s commercial automotive vertical and NAB powered by Plenti product (see further below)offset by softer results in consumer automotive lending.

Record quarterly renewable energy loan originations of $68 million were achieved, up 30% on PCP and up 4% on the prior quarter. Growth continued to be supported by Federal and State government incentive programs, with the WA Rebate BatteryScheme being a key driver of the result with over 7,500 rebates processed during the period.

Personal loan originations were $157 million, down 2% on PCP and 5% on the prior quarter with seasonal effects, pricing and competition and consumer demand impacting the quarter.

Margins

Plenti continued to increase its customer loan pricing to offset higher funding costs on new originations during the quarter, although average margins on new originations in the quarter were slightly lower than the prior quarter at ~5.4%.However, the impact of slightly lower margins on new originations was offset by strong outcomes on warehouse funding renewals and ABS transactions, meaning the overall portfolio net interest margin in 4Q26 was stable on the prior quarter and above the 1H26 level.

NAB partnership

The “NAB powered by Plenti” (NPBP) car loan continued to build momentum in 4Q26, with average originations per business day increasing 35% on the prior quarter. The result reflected ongoing collaboration between Plenti and NAB to implement initiatives to drive top-of funnel demand and improve conversion rates.

The NPBP loan portfolio increased to $121 million from $90 million at the end of the prior quarter, representing portfolio growth of 34% quarter-on-quarter.

Technology

Plenti continued to invest in its proprietary digital platform in the quarter to enhance customer experiences and drive business efficiency.

End-to-end control of the technology environment supports effective AI usage at Plenti with numerous AI driven initiatives recently implemented. This included a new front-end digital loan journey designed and deployed 70% faster than historic benchmarks using AI-assisted development tools. The new journey design supports faster ongoing updates and better funnel analytics to allow continual refinement of the customer experience.

In loan processing, Plenti’s DocAI platform assessed over 35,000 customer and partner-supplied documents during the quarter. This capability is improving processing efficiency, supporting higher levels of straight-through loan processing, and enhancing the customer and partner experience.

Plenti also deployed a new agentic AI platform in the quarter which supports use cases across the business. Initial applications include agents to assist customer service and sales engagement efficiency. An ongoing program of process automation is planned, which is expected to deliver uplifts in the speed and efficiency of technology delivery in FY27 and support operating leverage as the business continues to scale.

Credit performance

Annualised net credit losses for the quarter were low at 96 basis points, slightly up on the very low91 basis points in the prior quarter and lower than 116 basis points in PCP. Plenti had 90+ day arrears of 42 basis points at the end of the quarter,broadly stable on 41 basis points at the end of the prior quarter and 43 basis points at the end of PCP.

The loan portfolio’s weighted average Equifax credit score increased to 850 at the end of 4Q26, from 849 at the end of 3Q26, reflecting Plenti’s continued focus on lending to prime credit customers.

Plenti remains alert to the potential credit implications of recent geopolitical and macroeconomic developments, but believes that its disciplined approach to credit and strong prime loan portfolio, position the business well even if economic conditions do deteriorate.

Funding

Plenti completed a $400 million personal and renewable energy loan ABS transaction in February 2026, the Plenti PL &Green ABS 2026-1. The transaction was Plenti’s sixth PL & Green ABS, and twelfth ABS overall with total ABS funding completed now exceeding $4.7billion.

The transaction saw a record number of investors participating for a Plenti ABS, with strong support from both domestic and offshore accounts including long-term relationship investors and a number of significant new investors. The weighted average margin on the transaction was1.15%, representing Plenti’s best pricing outcome for any PL & Green transaction to date and 25 basis points tighter than the most recent prior PL& Green transaction completed in May 2025.

Plenti repaid $12.5 million of corporate debt in the quarter, reducing the drawn balance of its corporate facility to $20 million.Notwithstanding the repayment of corporate debt, strong operating cash generation and release of capital from funding transactions saw Plenti’s available corporate cash balance increase at period end from the balance at 30September 2025.

Further information

All numbers in this release are preliminary and unaudited. This release was approved by the Plenti Board of Directors.

Note: Plenti loan portfolio and origination numbers inthis release include “NAB Powered by Plenti” automotive loans