3Q26 update

.jpg)

Financial highlights

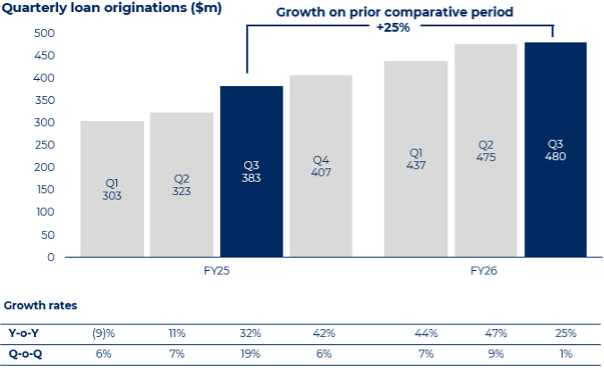

- Fifth consecutive quarter of record loan originations at $480 million, 25% above PCP and 1% above prior quarter despite 3Q26 having 5% fewer business days than 2Q26

- Loan portfolio increased to $2.98 billion, 24% above PCP and 5% above prior quarter

- Strong credit performance with annualised net credit losses of 91 basis points, down from 103 basis point in PCP and 94 basis points in the prior quarter

- 90+day arrears remained low at 41 basis points at quarter end, down from 47 basis points at the end of PCP and broadly consistent with the prior quarter at 39 basis points

- Revenue of $79.9 million, 22% above PCP – run-rate annual revenue of $320 million

- Completed $559 million automotive ABS transaction, Plenti’s largest securitisation deal to date achieving tightest pricing since 2021, bringing total issuance to over $4.3 billion

In addition, in the past week, Plenti achieved its FY26 objective of hitting a $3 billion loan portfolio, substantially ahead of the original target date of 31 March 2026.

Commenting on the quarter, Adam Bennett, Plenti’s Chief Executive Officer said:

“Plenti has delivered another exceptional quarter, achieving a fifth consecutive quarterly loan originations record of $480 million. I’m extremely pleased with the results that Plenti is delivering, leveraging our differentiated data, technology and credit capabilities alongside our focus on deepening our relationships and partnerships. In addition to very strong third quarter results, it has been fantastic to hit our FY26 loan portfolio target of $3 billion, well ahead of our original anticipated timing. This was an ambitious strategic goal when we set it in early calendar 2025 and achieving it in January 2026 is a testament to the hard work of the entire Plenti team.”

Loan portfolio

Plenti’s loan portfolio increased to $2.98 billion at 31 December 2025, a 24% increase from 31 December 2024 and a5% increase from 30 September 2025. The loan portfolio remains diversified across Plenti’s three lending verticals, each of which delivered strong and consistent growth against the prior corresponding period (PCP) and prior quarter.

Loan originations and margins

Overall originations result

Loan originations for the quarter totalled $480 million, 25% above PCP and1% above the prior quarter. The third quarter also had 5% fewer business days than 2Q26 resulting in a more material uplift in the per business day run-rate.

Product level originations

Automotive loan originations were $250 million, up 29% onPCP, and down 5% on the prior quarter. Performance in the period was particularly strong in the commercial automotive channel with increases in both active referring brokers and loan share of large referrers driving solid growth.This offset a reduction in the more volatile electric vehicle (EV) lending channel.

Record quarterly renewable energy loans of $65 million were up 33% on PCP and 14% on the prior quarter. As expected, growth was supported by government incentive programs, including the federal Cheaper Home Batteries Program and the WA Battery Scheme, which increased demand for solar and battery systems. While market feedback suggests battery supply has improved to meet demand, constraints remain in availability of resources to install systems, creating growth potential as installation capacity grows.

Personal loan originations were $165 million, up 18% onPCP and 8% on the prior quarter. Growth was particularly strong in direct channels where technology improvements to API integrations with affiliates and enhanced borrower journeys for customer re-lend continue to deliver results. Plenti also invested in operational capacity to continue to support fast and efficient loan processing in the period.

Margins

From mid-October to mid-December there was a ~50 basis points increase in the market component of Plenti’s funding costs, driven by a change in expectations regarding future RBA rate decisions.As a result of this change, Plenti saw a ~14bps reduction in the average margin on new originations in 3Q26 against 2Q26.

Plenti responded to the change in market funding costs with adjustments to customer pricing through December and by January had recovered ~25bps of margin through pricing changes.Pleasingly, application and origination volumes have remained robust not withstanding the price changes implemented. Plenti is continuing to monitor both funding costs and market competitive dynamics to assess opportunities to recover further margin in the current quarter.

Given the size of Plenti’s existing loan portfolio, which is continually hedged against market swap cost fluctuations, the impact of variance in margins on new originations for a few months is relatively minor. The overall loan portfolio margin was also supported by benefits from improved warehouse pricing agreed in recent months and completion of the automotive ABS transaction in November 2025.

NAB partnership

The “NAB powered by Plenti” car loan portfolio increased to $90.1 million at the end of 3Q26 from $66.7 million at prior quarter end. While this represented portfolio growth of 35%quarter-on-quarter, the value of daily originations for the product was flat across the two periods. A number of initiatives were launched in December aimed at driving increased application volumes and improved conversion rates, which are delivering benefits. Plenti and NAB have agreed a further set of initiatives for the coming quarters designed to accelerate loan originations.Some of these initiatives are likely to involve investment from Plenti to support growth.

Credit performance

Annualised net losses for the quarter were low at 91 basis points down from 103 basis points in PCP and 94basis points in the prior quarter. 90+ days arrears also remained low at 41basis points, down from 47 basis points at the end of December 2024 and only marginally up from 39 basis points at the end of the prior quarter. This strong result reflects the credit strength of Plenti’s prime loan portfolio as well as stable macroeconomic conditions in the period.

The loan portfolio’s weighted average Equifax credit score remained high at 849 at the end of 3Q26, consistent with 849 at the end of 2Q26, reflecting Plenti’s continued focus on lending to prime credit customers.

Funding

Plenti completed a $559 million automotiveloan ABS transaction in November 2025. The transaction was the largest securitisationdeal for Plenti to date with strong investor demand driving the tightestpricing achieved since 2021, despite significant volume of competing supply inprimary debt markets. The weighted average margin on the notes of 1.02% was materially lower than the 1.24% weighted margin achieved in the Automotive 2025-1ABS in early 2025.

This transaction was Plenti’s sixth automotive loan ABS and eleventh ABS transaction overall, with total issuance across Plenti’s public securitisation programs now exceeding $4.3billion.

FY26 objectives

Plenti’s objectives for the year to 31 March 2026 are set out below. Very pleasingly, the $3 billion loan portfolio growth has already been delivered in January2026. Strong loan portfolio growth and stable credit along with measured business investment has continued to see business profitability improve in3Q26, supporting the objective for second half Cash PBT and Cash NPAT growth. Plenti also remains on track to meet the efficiency objective.

Resignation of Chief Financial Officer

The Board of Plenti today also advises that Miles Drury has resigned as Chief Financial Officer. Miles has been with Plenti for six years, working to IPO Plenti in September 2020, and helping to guide our business through a period of significant growth and change. Miles will continue in the CFO role during his four-month contractual notice period to ensure an orderly transition, and to deliver our full year FY26 results in May 2026.

Adam Bennett, CEO of Plenti said:

“I’d like to acknowledge Miles’ contribution to all aspects of our business over the last six years, and thank him for his hard work, commitment, strategic leadership and his contribution to the Company’s development and profitable growth over Plenti’s formative years.

“I’ve enjoyed working with Miles over the last 18 months and I know how instrumental he’s been in building Plenti’s highly skilled treasury, commercial, financial management and investor relations capability. We now have a highly experienced team of specialists in place that will continue to support Plenti’s scaling and growth, and full credit goes to Miles for building this out.

“We wish Miles every success in his future endeavours.”

A comprehensive search for are placement CFO with appropriate commercial, financial services and ASX-listed experience is well advanced, and we expect to make an announcement regarding the appointment of Plenti’s new CFO next week.

Further information

All numbers in this release are preliminary and unaudited. This release was approved by the Plenti Board of Directors.

Note: Plenti loan portfolio and origination numbers in this release include “NAB Powered by Plenti” automotive loans