1H26 update - Plenti delivers exceptional profit growth

.jpg)

Financial highlights

- Cash PBT of $14.1 million, representing an increase of 147% on pcp

- Cash NPAT of $12.8 million, representing an increase of 133% on pcp

- Loan originations of $912 million, up 46% on pcp

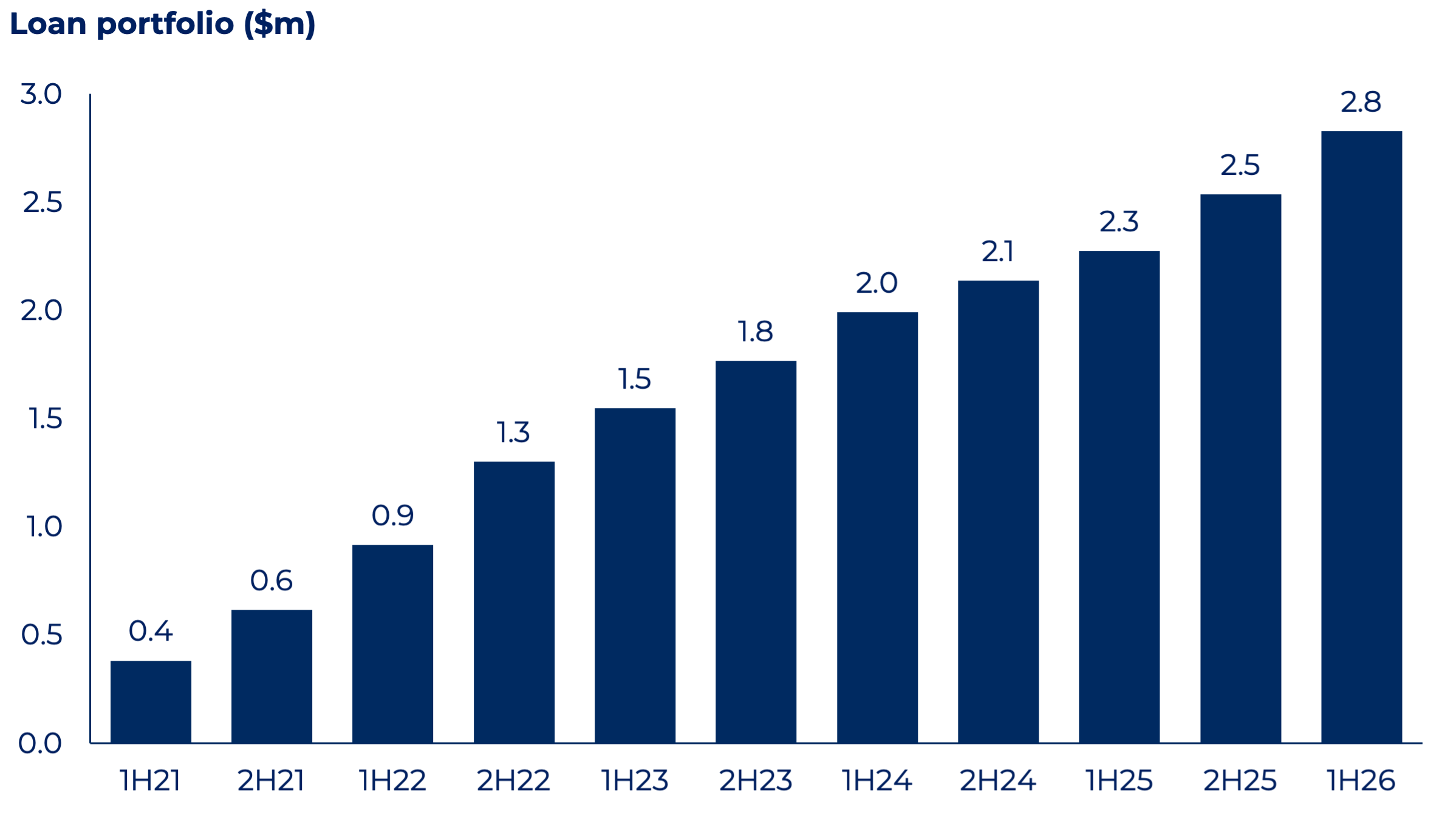

- Closing loan portfolio of $2.83 billion, up 24% on pcp

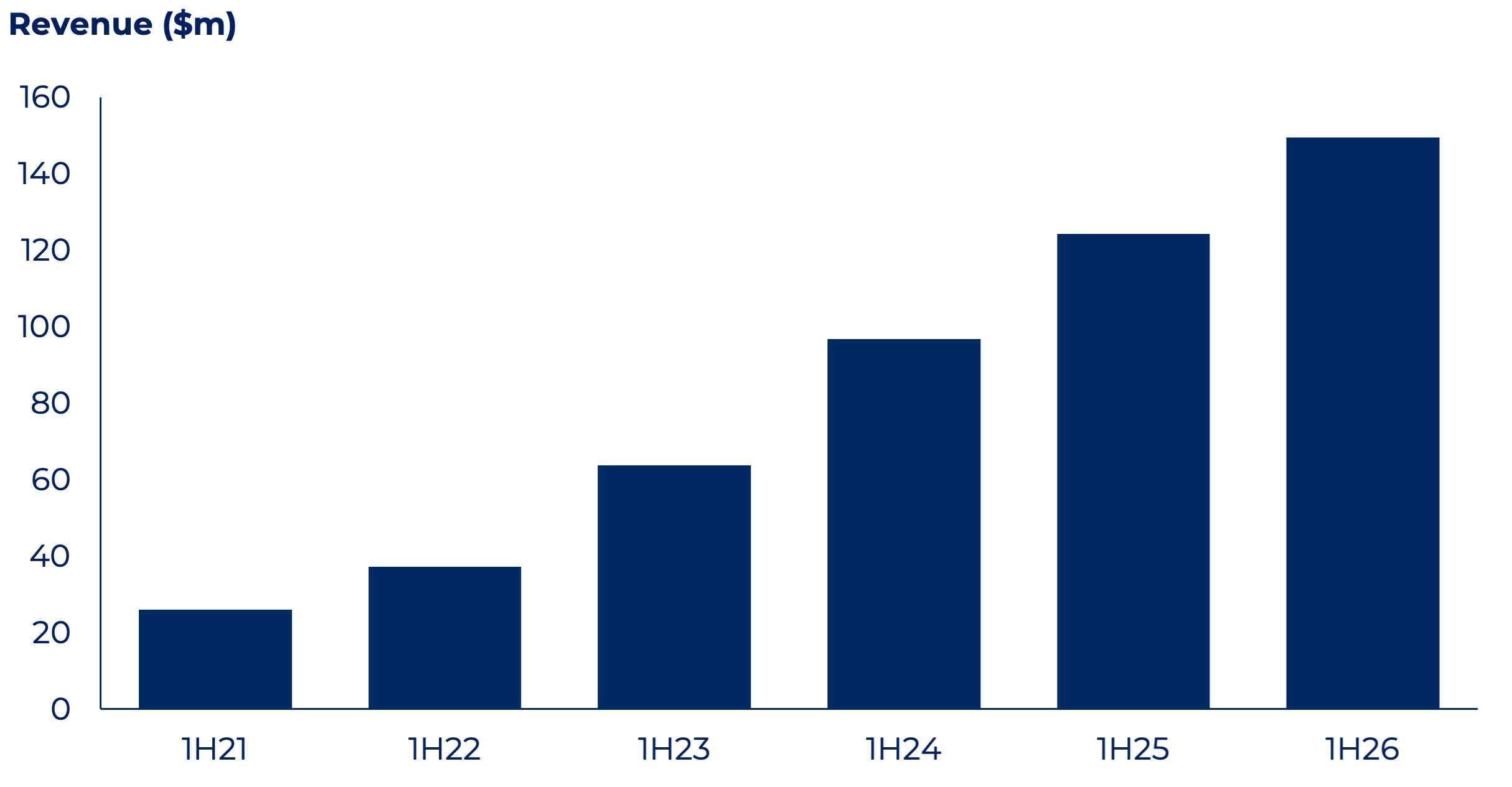

- Half-year revenue of $149.5 million, up 20% on pcp

- Exceptional credit performance, with a 0.94% annualised net credit loss rate and 90+ days arrears rate of 39bps1 at period end (down from 50bps in pcp)

Operational highlights

- Achieved further consecutive record quarters of loan originations in1Q26 and 2Q26, with momentum across all lending verticals

- Won and launched the WAResidential Battery Scheme, deploying the end-to-end technology solution inless than six weeks during 1Q26, reinforcing our leadership in household clean energy finance

- Delivered further advancements to Plenti’s proprietary technology platform, including significant enhancements to automated“straight through processing” credit approvals

- Completed $400million PL & green asset-backed securities (ABS) transaction as well as priced a $559 million automotive ABS transaction (post period end) at tight margins, bringing total ABS issuance to over $4.3 billion

Strategic highlights

- Continued to build momentum in the “NAB powered by Plenti” car loan product, with the loan portfolio reaching $67 million in September 2025

- Successfully delivered onHorizon 1 (GROW by doing what we do but better) of our breakout growth strategy, remaining on track for a $3 billion loan portfolio by March 2026

Commenting on the quarter, Adam Bennett, Plenti’s Chief Executive Officer said:

“Plenti delivered an exceptional first half, underpinned by continued operational execution and the compounding effect of our technology-led model. Achieving a fourth consecutive record quarter of originations in 2Q26 propelled us to $912 million in originations for the half, representing 46% growth on the prior year.

This strong performance has translated directly into meaningful profitability growth, demonstrated by 1H26 Cash PBT of $14.1 million and Cash NPAT of $12.8million, increases of 147% and 133% respectively on 1H25."

Loan portfolio and loan originations

Plenti’s diversified loan portfolio increased to $2.83 billion at 30 September 2025, up 24% from the prior comparable period (pcp) and up 12% from 31 March 2025.

Total loan originations for the half were $912 million, up 46% on pcp. This comprises 1Q26 originations of$437 million and 2Q26 originations of $475 million.

Revenue and profitability growth

Plenti generated half-year revenue of $149.5 million, representing 20% growth on pcp, driven by the expansion of the average loan portfolio and stability in customer rates.

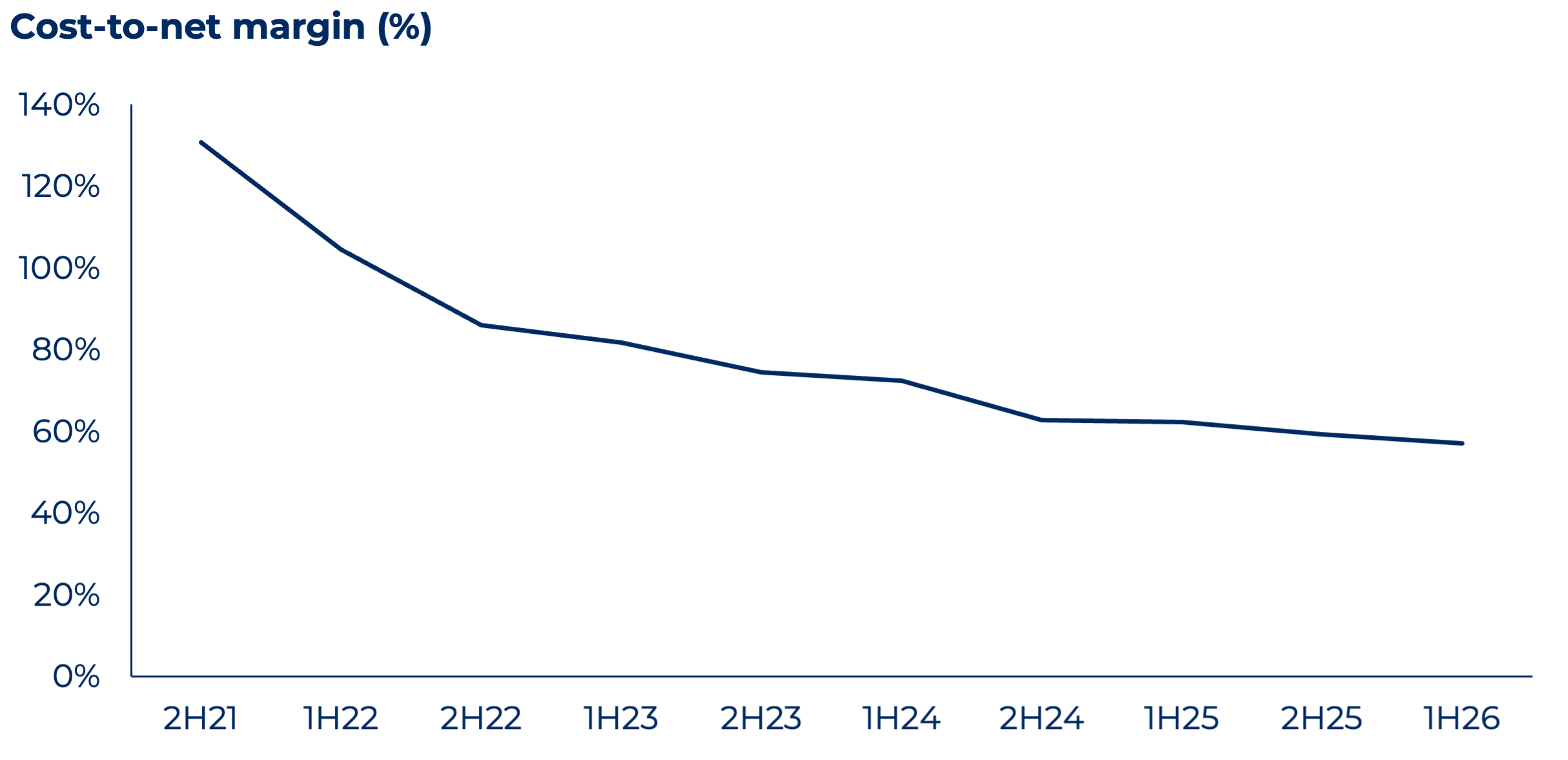

Strong loan book growth, effective management of loan margins, and low credit losses, combined with ongoing operational efficiency, translated into the strong profitability results with Cash PBT of $14.1 million and Cash NPAT of $12.8 million. Given the level of profitability achieved, Plenti anticipates that all available carried forward tax losses will be utilised during FY26, resulting in some cash tax being payable by the group.Accordingly, a $1.3 million provision for cash income tax has been included in the 1H26 result.

Technology enhancements

Plenti continued to invest in its proprietary technology platform to further differentiate the business, enhance customer experiences and drive operational efficiency. During the period Plenti:

- Deployed pilots of artificial intelligence (AI) technologies, including an AI assistant environment to support frontline and back-office teams, AI co-pilots to assist software development, and document verification experiments to streamline loan origination. Plenti's AI investment is expected to continue to ramp in 2H26, including further deployment of a gentic AI to support efficient originations and servicing

- Supported the launch of the Western Australia Residential Battery Scheme, a rebate and interest-free loan scheme for home batteries. Highlighting the agility and integration capabilities of Plenti's platform, the project moved from concept to a fully operational financing solution in approximately six weeks. This rapid deployment of a high-impact initiative underscores the flexibility and integration capabilities of Plenti's platform and validates our ability to partner and deliver complex programs at pace

Consistent with prior periods, all investment in product and technology during 1H26 was expensed through the profit and loss statement.

Credit performance

Plenti delivered another very strong half of credit performance, reflecting the prime nature of its loan portfolio. The annualised net credit loss rate for the half year was 0.94%.

90+ day arrears reduced materially to 39 basis points at the end of the period, down from 50 basis points at 30 September 2024. This reflects the credit strength of Plenti’s prime portfolio and a focus on proactive credit management. The loan portfolio weighted average Equifax credit score remained high at 849.

Financial position and funding

Plenti continued its programmatic approach to funding, successfully completing a $400 million PL & Green ABS debt transaction in May 2025. On 14November 2025, Plenti also successfully priced a further $559 million secured automotive ABS transaction, bringing lifetime ABS issuance for Plenti to over$4.3 billion. Structured credit markets in Australia continue to be very robust with a weighted average note margin on the PL & Green transaction of 1.40%and a weighted average margin for the auto transaction being 1.02%. The automotive ABS pricing represented the lowest cost ABS Plenti has completed since2021.

InOctober 2025, Plenti also established a new warehouse funding facility with a global investment bank and a large domestic credit investor to fund both secured and unsecured loan products. The new facility is competitively priced andhas an initial limit of approximately $350m, with potential to upsize, providing additional funding scale and diversity to support the origination growth ambitions of the business.

Plenti funded its operations from business cashflows during the period. Net equity invested into securitised funding structures to support on-balance sheet loan portfolio growth of $245m in the period was $7.5 million. This amount wasfunded through operating business cashflows.

Update on FY26 objectives

Plenti has made strong progress executing on Horizon 1 of its refreshed strategy over the first 6months of FY26 and remains well on track to achieve its objective of a $3billion loan portfolio by March 2026.

Plenti’s objectives for the year to 31 March 2026, as updated in the 2Q26 trading update in October 2025, are set out below:

Plenti remains on track to deliver these objectives.

Further information

This release was approved by the Plenti Board of Directors.

1. This value has been updated against the 35bps reported at 2Q26 – due to a system reporting issue the value was initially slightly understated, which was identified through review and reconciliation procedures for the month

2. Plenti loan portfolio and origination numbers in this presentation include “NAB Powered by Plenti” automotive loans