4Q25 update - Momentum accelerates

Plenti Group Limited (ASX:PLT) (Plenti) provides this trading update for the quarter ended 31 March 2025 (4Q25).

Highlights

- Record quarterly loan originations of $407 million, up 42% on PCP and up 6% on prior quarter, despite Q4 typically being a seasonally weaker quarter

- Loan portfolio increased to $2.5 billion, up 19% on PCP and up 6% on prior quarter, reflecting strong growth in originations across all lending verticals

- Annualised net credit losses of 116 basis points, against 103 basis points in the prior quarter

- 90+ day arrears of 43 basis points at quarter end, down from 47 basis points at the end of the prior quarter

- Quarterly revenue of $69.4 million, up 16% on PCP

- $509 million secured auto ABS transaction completed, Plenti's largest ABS to date with very strong investor support driving favourable pricing outcomes

- Unaudited H2 Cash NPAT of $8.3 million, resulting in full year FY25 Cash NPAT of $13.8 million, representing 126% growth on FY24

- FY25 market guidance objectives for growth, profitability and efficiency delivered

Note: Plenti loan portfolio and origination numbers in this release include 'NAB Powered by Plenti' automotive loans

Commenting on the quarter, Adam Bennett, Plenti's Chief Executive Officer said:

“This was another outstanding quarter for Plenti, with quarterly originations exceeding $400 million for the first time, driven by excellent momentum from all three of our lending verticals. The record result was particularly impressive given that lending was impacted by Cyclone Alfred for part of March. Combined with ongoing strong credit performance and cost discipline, it's very pleasing to see our originations and loan book momentum delivering a strong increase in full year Cash NPAT to $13.8 million and setting us up well for continued profit growth in FY26.”

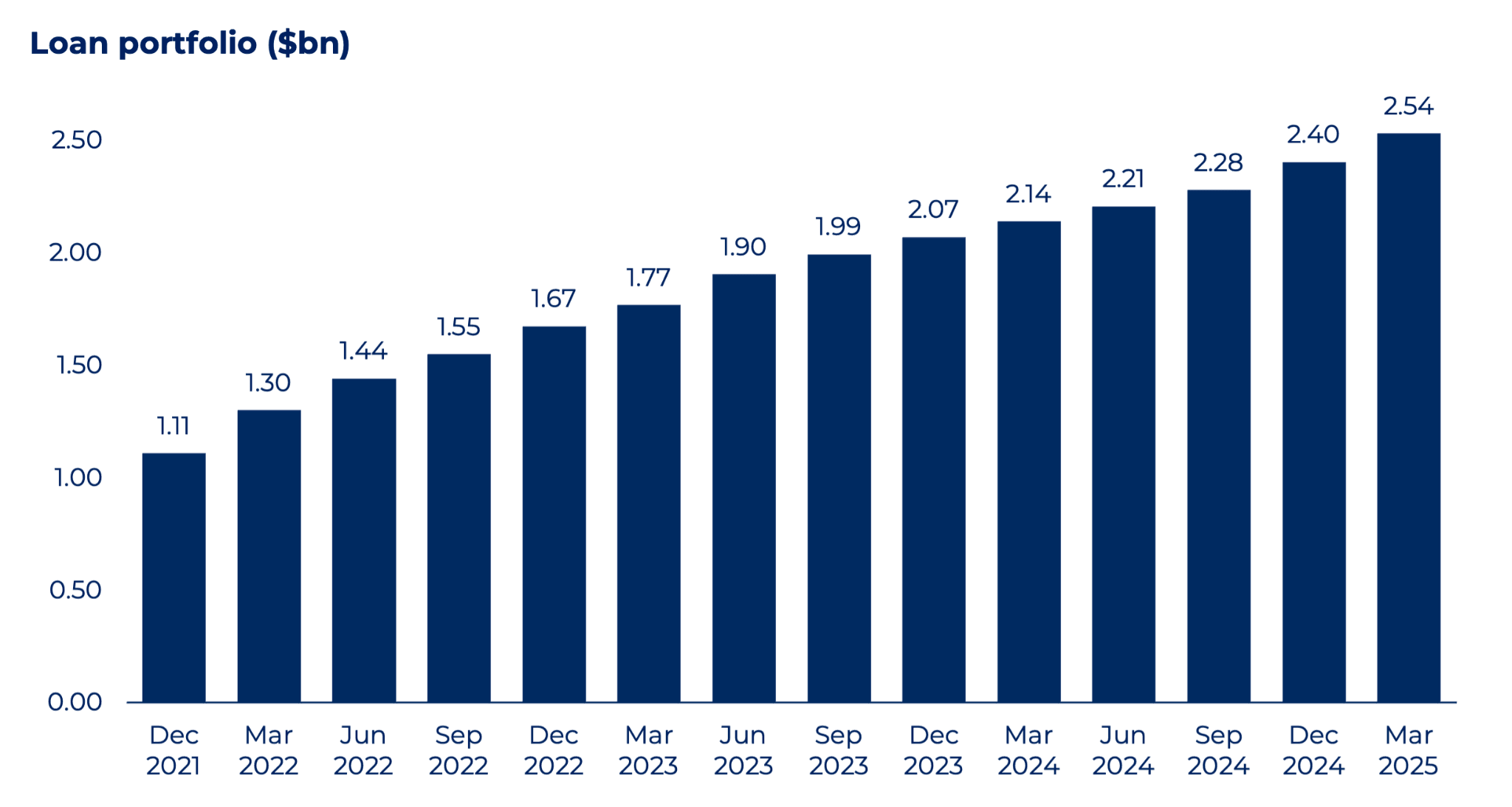

Loan portfolio

Plenti's loan portfolio, which is a key driver of revenue and profitability, increased to $2.5 billion at 31 March, a 19% increase from 31 March 2024 and a 6% increase from 31 December 2024

| Loan portfolio by product ($m) | 31 Mar 24 | 31 Mar 25 | Growth |

| Automotive | 1,223 | 1,431 | 17% |

| Renewable energy | 273 | 341 | 25% |

| Personal | 643 | 764 | 19% |

| Total | 2,138 | 2,537 | 19% |

Loan originations and margins

Plenti delivered record loan originations in the quarter of $407 million, up 42% on prior corresponding period (PCP) and up 6% on the prior record in the preceding quarter. The growth achieved on Q3 was particularly notable given Q4 is typically a seasonally weaker quarter – the prior two financial years have each seen a loan originations decline in Q4 against Q3.

Automotive loan originations were $195 million, up 35% on PCP and broadly consistent with the prior quarter. Solid growth was achieved in both core consumer and commercial offerings against the prior quarter, offsetting a reduction in EV lending as the Tesla subvention offer concluded. Strong loan originations were supported by continued operational excellence in loan processing, delivering rapid loan approvals and efficient settlement processes for brokers and referrers.

Record quarterly renewable energy loan originations of $52 million were achieved, up 27% on PCP and up 6% on the previous quarter. Origination growth continued to be supported by Plenti's unique market-leading GreenConnect platform driving home battery uptake.

Record personal loan originations of $160 million were achieved, up 58% on PCP and up 14% on the prior quarter. The result reflected solid demand, increased investment in digital acquisition channels and further advancements in automated credit approvals as well as increased repeat and cross-sell origination volumes from existing borrowers.

Overall net interest margins on new loan originations were broadly stable on the prior quarter.

NAB partnership

The 'NAB powered by Plenti' (NPBP) car loan was made available to NAB customers in late September 2024 and had been expected to contribute only moderate volumes in 2H25. Important work was completed in 4Q25 to increase the visibility of the product to NAB customers, with the NPBP car loan made available via the NAB website, NAB banking app and internet banking portal. Some initial marketing campaigns were also undertaken in the period with further NAB investment planned in the coming quarter.

While volumes are growing from a low base, originations in 4Q25 were up over three times from 3Q25 and March originations were up 60% on the preceding month. At 31 March 2025 the NPBP car loan contributed $16.7 million to the loan portfolio balance, in line with both Plenti's and NAB's expectations.

Credit performance

Annualised net losses for the quarter were 116 basis points, up from a seasonally low 103 basis points in the December quarter and broadly consistent with preceding quarters.

Plenti saw an improvement in arrears in the period with 90+ day arrears of 43 basis points at the end of the quarter, down from 47 basis points at the end of the prior quarter. This is a notable outcome because seasonal trends would typically drive arrears upwards into March before then moderating in the middle of the calendar year.

The loan portfolio weighted average Equifax credit score remained high at 846 at the end of 4Q25, versus 845 at the end of 3Q25, reflecting Plenti's continued focus on lending to prime credit customers.

Funding

Plenti completed a $509 million automotive loan ABS transaction in February 2025, its largest ABS transaction to date. Completion of the deal brought total ABS issuance for FY25 to $1.3 billion with cumulative lifetime issuance of ABS by Plenti now over $3.4 billion.

The transaction was the first securitisation deal to price in the Australian market for 2025, and attracted strong demand, with a record number of investors participating in the transaction. The volume of investor demand supported Plenti in improving pricing through the marketing process to achieve a result below that of comparable peer transaction pricing at the end of 2024, and ~25bps inside the comparable Plenti automotive ABS transaction in 2024.

FY25 objectives and Cash NPAT result

Plenti delivered unaudited Cash NPAT in 2H25 of $8.3 million, bringing the full year FY25 unaudited Cash NPAT result to $13.8 million. This represents growth of 126% on FY24.

Plenti's strong originations momentum in Q3 and Q4 and the significant Cash NPAT growth achieved ensured that the business delivered on its FY25 objectives as set out below.

| Priority | FY25 objective |

| Growth | - Drive growth in loan originations and loan portfolio |

| Profitability | - Continue profitability momentum to deliver full year and half-on-half Cash NPAT growth |

| Efficiency | - Reduce cost-to-income ratio to <24%- Remain on target to deliver $25m in efficiencies as loan portfolio scales from $1.5 billion towards $3 billion |

Further details in respect of FY25 and outlook for FY26, will be provided when Plenti reports its full financial year result on Wednesday 21 May 2025.

Further information

All numbers in this release are preliminary and unaudited. This release was approved by the Plenti Board of Directors.